Blog

-

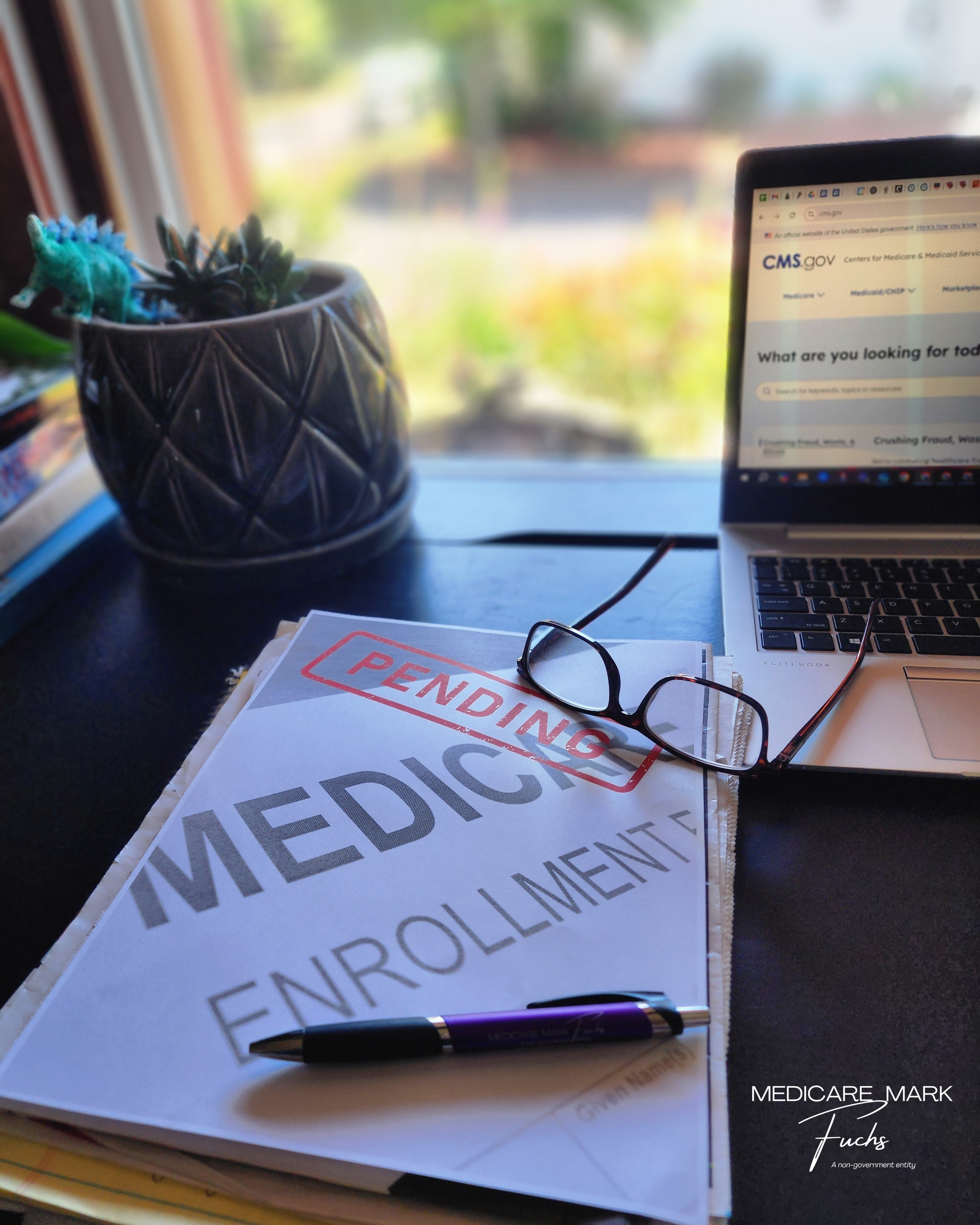

Currently, delays at the Centers for Medicare & Medicaid (CMS) are causing carrier applications to go pending, giving the potential for coverage start dates to be delayed.

We have no insight into the inner workings of CMS, so we can only report on what we have experienced and confirmed with some of our contracted carriers.

This post serves to inform you, not alarm you. Read on for information and recommended action…

What’s Happening:

We’ve confirmed with multiple insurance carriers that new enrollments are showing as “pending” due to slower turnaround times at the Centers for Medicare & Medicaid Services (CMS). This is not typical.

Normally, once a plan application is submitted, it moves through the process quickly. But right now, things are taking longer — and it’s impacting when coverage actually begins.

Why This Matters:

If you're new to Medicare, the delay could mean a gap in your coverage if you don't plan ahead.

Your Medicare enrollment window is seven months:

Three months before your 65th birthday (or retirement date if you're already over 65)

The month of your birthday

And three months after your birthday

However - with CMS running behind, you can’t assume that submitting your paperwork even weeks in advance is enough.

Our Strong Recommendation: Whether enrolling in Original Medicare (Parts A & B), a Medicare Supplement plan, or a Medicare Advantage plan, give yourself AMPLE time.

👉 For those over 65, still working, planning to retire, and currently covered under employer insurance: We recommend starting the process of applying for Part B a full SIX MONTHS before your planned retirement. This allows for:

SSA processing time (also currently slower than normal)

CMS lag in approving and activating coverage

Ensuring the plan of your choice is in place when you need it

The punchline? Don’t wait - start early, secure your coverage, and protect your peace of mind.

If you're unsure of your timeline or would like to talk through your plans, book a time to talk here.

-

Providence Health Plans released an update on May 20 announcing their transition out of most lines of their health insurance business, beginning in 2027.

Life is 10% what happens to you and 90% how you respond to it.

-Charles Swindoll

This quote applies a lot to Medicare and the insurance business overall. We are following the Providence exit closely and are prepared to be in response - not react - mode, come fall and Annual Enrollment.

Check back at the Providence link to keep updated, and schedule an appointment anytime to discuss. There is always a pivot.

Link to article: Providence Update

Link to book a meeting: Meet with Mark

-

2026 standard monthly Part B premiums: $202.90 (an increase of $17.90 from $185.00 in 2025 - this does not include IRMAA, if applicable.)

2026 annual Part B deductible: $283 (an increase of $26 from the annual deductible of $257 in 2025.

Visit https://www.cms.gov/newsroom/fact-sheets/2026-medicare-parts-b-premiums-deductibles to see the full list of changes for 2026 pricing.

-

Patients of The Oregon Clinic are currently receiving letters stating the following:

“The Oregon Clinic will not be able to see UnitedHealthcare Medicare Advantage plan members starting January 1, 2026. Patients undergoing certain types of treatment may be eligible for continuity of care benefits. Please reach out to UnitedHealthcare to learn more about continuity of care.”

If you are affected by this sudden and impactful decision to our seniors, please reach out. It is imperative that you understand exactly what this means for your coverage and your care.

Schedule a consultation today to understand your options for 2026.

-

Samaritan has announced that it is ending its Medicare Advantage plans in Oregon at the end of 2025.*

While carriers leaving an area isn’t a new concept, it can still be a surprise to those who receive the notices, and leave them feeling unsure of what to do next.The potential silver lining: When a plan leaves an area, options become available that you may not be aware of, and we are here to guide you candidly and honestly through those options.

Having all available information in order to make to make informed decisions on your healthcare is paramount. To support this effort, we have added three events for Lincoln County, OR, residents during the Annual Enrollment Period:Sat. 10/25, 9:00-10:00am, Cafe Chill in Waldport

Sat. 10/25, 12:00-8:00pm, Yachats Commons

Sat. 11/8, 9:00-10:00am, Cafe Chill in Waldport

Add these meetings to your calendar from our events page.

Topics we will cover:

Remaining Medicare Advantage options

Supplement (MediGap) plans

Utilizing only Original Medicare (Parts A&B)

Come learn what is available to you in Lincoln County for 2026.

*https://philomathnews.com/samaritan-health-dropping-medicare-advantage-plans-at-end-of-year/ -

We’re shining a light on an important issue: many beneficiaries encounter unexpected bills, often leading to frustration and confusion. It can feel like companies rely on individuals not having the information or energy to challenge them. That’s where we come in.

Read on to empower yourself with essential knowledge about balance billing, also known as surprise billing…

What is Balance Billing?

Balance billing, or surprise billing, happens when healthcare providers charge you the difference between their fees and what your insurance covers. This often occurs unexpectedly, especially in emergencies or when receiving care from out-of-network providers at in-network facilities.Protections Under the No Surprises Act (Effective January 1, 2022)

The No Surprises Act, part of the Consolidated Appropriations Act of 2021, provides essential protections:

Emergency Care: All emergency services are treated as in-network, regardless of the provider, with no prior authorization needed.

Non-Emergency Services: If you receive care at an in-network facility but can’t choose your provider, you cannot be balance billed.

Air Ambulance Services: Similar protections apply, preventing balance billing from out-of-network air ambulance providers.

Dispute Resolution: Payment disputes between providers and insurers are resolved through an Independent Dispute Resolution (IDR) process, keeping you out of the conflict.

Positive Impact So Far

A 2024 survey found that the No Surprises Act prevented over 10 million surprise bills in the first nine months of 2023, with nearly 80% of out-of-network providers accepting initial in-network payments from insurers.

Medicare Beneficiaries and Balance Billing

Original Medicare: Strictly prohibits balance billing. Providers who don’t accept assignment can only bill you up to a capped amount, and private contracts require your consent in advance.

Medicare Advantage Plans: Offer similar protections against surprise billing in emergencies or when referred by in-network providers.

What You Can Do

Know Your Rights:

Emergency and air ambulance services are always billed as in-network.

Out-of-network care at in-network facilities is protected.

Decline Network Waivers:

If presented unexpectedly, especially during emergencies, do not sign them.

Review Your Explanation of Benefits (EOB):

If you receive a surprise bill, file a complaint with CMS or your State Insurance Commissioner, and consider appealing under the No Surprises Act.

Consult Your Broker:

A knowledgeable advisor can help you navigate these rules and ensure you’re informed of your rights.

Current Landscape for Beneficiaries

As of this writing, no federal changes are expected that would weaken balance billing protections for Medicare or Medicare Advantage enrollees. In fact, Congress is considering stronger enforcement laws, and the Centers for Medicare & Medicaid Services (CMS) is enhancing dispute resolution processes and improving hospital billing transparency to further support beneficiaries.

Bottom Line

The No Surprises Act and Medicare regulations provide strong safeguards against balance billing. Recent policy updates continue to reinforce these protections. Navigating complex healthcare billing can be challenging, so having a dedicated broker year-round is essential to avoid unexpected costs.

If you receive a surprise bill, don’t pay it immediately. Reach out to us; we’ll review your coverage together, then guide you through the next steps.

Need help with a bill you’ve received or with understanding your rights? Book an appointment - we provide support all year, not just during enrollment season!

-

Across the country, UnitedHealthcare is cutting commissions for brokers and agents on Institutionalized Special Needs Plans (ISNPs) and $0 premium Medicare Advantage plans—plans used by the most vulnerable seniors in our community.

We have always been upfront about how the Medicare system works—including how we get paid. It’s part of our commitment to transparency, trust, and ethics. So when something happens that threatens the integrity of that system—and our ability to serve you well—we speak up.

Recently, a national advocacy organization, NABIP, issued a strong public statement about UnitedHealthcare’s decision to slash commissions for Medicare Advantage plan enrollments in several markets across the country. We support NABIP’s message 100% and want to explain what this could mean for our Oregon clients if these cuts expand to our state.

What’s Happening?

UnitedHealthcare, one of the largest Medicare Advantage plan sponsors, has reduced how much it pays independent brokers like us to help enroll and support members in their plans. These changes have already taken effect in other states, and there is concern that Oregon could be next.

This move may sound like an internal business decision—but it has real consequences for you, the Medicare beneficiary.

Why Should You Care?

Brokers and agents don’t just enroll people in plans. We…

Walk you through complex coverage options

Help you understand drug formularies, networks, and out-of-pocket limits

Assist with claims issues, prior authorizations, and billing errors

Are your advocate year-round, not just during Annual Enrollment

When commissions are cut too low, fewer professionals can afford to offer that level of service, potentially leading to:

Fewer local brokers offering support on certain plans

A shift toward high-pressure, national call centers instead of personalized help

Seniors being left to figure things out on their own, often with confusing or misleading information

We are a small, community-rooted business. We don’t charge for our help; our compensation comes from the plan sponsors (see the explanation here). But if those sponsors cut rates to the point where brokers can’t operate sustainably, it chips away at the very foundation of Medicare advocacy.

What This Means for Our Clients

We aren’t going anywhere. We will always tell you the truth about what’s changing in the industry. If UnitedHealthcare or any other plan reduces our ability to serve you effectively, we’ll be honest about it and help you navigate other options. We’ll continue to educate, advocate, and support the people who trust us with their Medicare journey.

We Support NABIP’s Call to Action

As NABIP members, we’re grateful for their leadership in standing up for the ethical, sustainable delivery of Medicare. We hope more people—clients, lawmakers, and carriers alike—pay attention to this issue before it becomes the new normal.

Final Thoughts

The Medicare system works best when seniors are informed and supported—and when agents are treated with fairness and respect. Our promise at Medicare Mark Fuchs LLC is to always operate with clarity, ethics, and your best interest at heart.

…What can I do?

—> Fill out this 5-question survey that NABIP developed to advocate with legislators on behalf of brokers and agents to recognize their value in working with Medicare beneficiaries. You have the option to remain anonymous!

—> If you have questions or concerns about your plan or how these changes might impact you, please don’t hesitate to contact us to book an appointment.

Serving Oregon’s Medicare community with integrity, transparency, and heart.

Read NABIP’s full statement here.

-

For many people 65 and older, Medicaid has been a lifeline—helping cover healthcare costs that Medicare alone doesn’t. Recently, we have seen a wave of people losing their Medicaid benefits. Whatever the reason - income changes, redetermination issues, or confusing paperwork, it’s creating real stress for seniors.

If you (or someone you know) has recently lost Medicaid coverage, you are not alone—and there are steps you can take to avoid losing health benefits or access to care.

Let’s walk through this:

Q: What Happens When You Lose Medicaid?

A: Losing Medicaid can affect your coverage in several ways:

Medicare Savings Programs: If Medicaid was paying your Part B premium (usually $185/month in 2025), you may now have to pay it yourself—unless you qualify for another savings program.

Extra Help (Low-Income Subsidy): If you received help paying for prescriptions through Medicaid, you may lose your Extra Help benefits too—meaning higher copays at the pharmacy.

Dual Special Needs Plan (D-SNP): If you were enrolled in a D-SNP, losing Medicaid can mean you’re no longer eligible for that plan, and could be disenrolled unless you take action.

Long-Term Care or Home Support: If Medicaid helped with long-term care or in-home assistance, losing coverage may affect those services.

Special Enrollment Period (SEP): You may be eligible for a special enrollment period to change your Medicare plan after Medicaid loss—but timing matters.

Q: This is really overwhelming. What can/should I do?

A: You can do these things right now:

Don’t Ignore Notices

Medicaid loss often happens after a redetermination. If you get a letter, open it—and bring it to us. We can help you understand it and respond.Check for Other Programs

You may still qualify for partial Medicaid or other programs like QI-1, SLMB, or LIS (Extra Help) that can ease the financial burden.Review Your Medicare Plan

If your Medicaid status has changed, your Medicare plan may need to change too—especially if you were in a D-SNP or had enhanced drug coverage.Act Quickly

You may qualify for a Special Enrollment Period, but it’s usually time-limited. Acting fast protects your access to care and keeps costs down.

We’ve helped dozens of Oregonians navigate the loss of Medicaid with clarity and compassion. Here's what we do:

One-on-One Help: We explain your options clearly and help you understand what’s changing—and why.

Plan Reviews: If your Medicaid is ending, we help you re-evaluate your Medicare plan to make sure you're not paying too much or missing out.

Timely Action: We track deadlines and Special Enrollment windows so you don’t have to.

This IS overwhelming. And - you are not alone. We are local, experienced, and here to help you make the best decisions with confidence and calm.

If you’re 65+ and just got a Medicaid termination letter—or are worried one is coming—schedule a review with us today.

Let’s talk through your options and get you set up with the coverage that fits your life now.👉 Book your appointment at www.calendly.com/medicaremarkfuchs/medicaid-loss.

Medicare Mark Fuchs LLC—local help, lifelong care.

-

First, what is a “final rule”?:

A “final rule” is Medicare’s way of saying, “We’ve made up our minds. This is how things will work next year.” (Remember ‘Who Wants to be a Millionaire’? This is CMS’s “Final Answer”.)

The purpose of the final rule is to ensure that everyone — from local pharmacies to nationwide insurance plans — is on the same page and following the same rules.

So - when you hear that CMS (Centers for Medicare & Medicaid Services) has issued a “final rule,” it means the government has made a decision about how certain parts of Medicare will work in the future.

Here’s how the process works:

CMS makes a proposal.

Called a “proposed rule”, CMS announces what they might change — for example, how much insurance companies get paid for Medicare Advantage plans, or what changes might be coming to drug coverage.They ask for public input.

Doctors, insurance companies, advocates — even everyday people — can send in their opinions during a designated timeframe. CMS reviews the feedback.CMS makes it official.

After considering the input, CMS releases a “final rule.” This is the version that becomes the law going forward. It includes all the important details that insurance companies and Medicare plans must follow in the coming year.

Why Should You Care About a Final Rule?

Because they tell us things like:

How Medicare plans will change.

What benefits might be added or removed.

How much the government will pay insurance companies.

Whether you might see more (or fewer) options in your area.

Final rules very much affect you and your coverage. When new plan information is released, or something has changed and you notice it in a doctor bill or at the pharmacy, is is very likely due to a CMS Final Rule.

Anytime you receive something that has you confused or questioning your coverage, schedule an appointment with Mark. He is happy to look at it with you and get to the bottom of your concerns.

-

If you receive Social Security benefits—including Medicare, Social Security Disability (SSDI), or Supplemental Security Income (SSI)—you may have heard about new identity verification requirements. These changes are designed to prevent fraud, and we combed through a notice on the SSA website to glean the important pieces as it pertains to Medicare beneficiaries (click here to see the full article).

Who Needs to Prove Their Identity?

For most people, nothing changes—you do not need to prove your identity unless:

✔️ You are applying for benefits for the first time.

✔️ You are changing your direct deposit information.If you are already receiving benefits and not making any changes, your payments will continue without any action on your part.

*** BENEFICIARIES BEWARE ***

Social Security will never text or call you to confirm your identity. If you receive a text or phone call asking for your information, ignore it—it’s a scam!

How to Prove Your Identity Securely

The easiest and safest way is by using a my Social Security account online.

If you are applying for Medicare or SSDI, you can verify your identity by phone.

If you are applying for retirement, survivors, or auxiliary benefits, or changing direct deposit information, you must visit a Social Security office in person.

Impact to Medicare Beneficiaries

If you receive Medicare benefits through Social Security, your payments will continue without any changes.

However - if you change your banking information, you will need to verify your identity using one of the approved methods.

If you have additional questions about how this impacts your Medicare coverage, reach out to Medicare Mark Fuchs for trusted guidance. We’re here to help you navigate these changes with confidence!

-

The Trump administration has officially ended efforts to launch a $2 generic drug discount program for Medicare enrollees. The program, initially developed under the Biden administration and first previewed in 2023, aimed to make about 150 common generic drugs available for just $2 per prescription. CMS officials estimated that this initiative could have benefited 32 million Medicare Part D enrollees, helping them save on essential medications. However, with the administration rescinding support for the project, the program will no longer move forward.

Key takeaways include:

No $2 generic drug list* under Medicare Part D.

Potentially higher out-of-pocket costs for common medications, plan-dependent.

Limited access to ultra-low-cost prescriptions - again, plan-dependent.

Continued reliance on plan formularies, which vary in coverage and pricing.

Unclear reasons for canceling the program or how much money CMS expects to save.

For Medicare beneficiaries, this means carefully reviewing your Part D drug plan is more important than ever. Many plans do offer low-cost generic drugs, but coverage varies widely.

With his expertise and access to 15 insurance carriers, Mark can help you navigate your options. If you’re concerned about drug costs or need a plan review, schedule a consultation today to ensure you have the right coverage for your situation.

*From CMS.gov: Medicare $2 Drug List Model List RFI Sample Drug List (RFI = Request for Information, which means these were drugs under consideration.)

-

The No Surprises Act, signed into law in 2020, was designed to protect Americans from unexpected medical bills. However, recent job cuts at the federal office responsible for overseeing this protection (the Center for Consumer Information and Insurance Oversight, or CCIIO) are creating uncertainty in how disputes between insurers and medical providers are handled.* While the core law remains in place, the impact of these cutbacks could mean:

Longer delays in resolving disputed medical bills.

Weaker enforcement of patient protections.

Potential cost increases as insurers and providers struggle with a backlog of cases.

Less support for consumers trying to file complaints about billing issues.

Uncertainty around new rules that were supposed to make the process more efficient.

For those on Medicare, this highlights an even greater need to understand your coverage and avoid unexpected costs. While the No Surprises Act primarily applies to private insurance, Medicare beneficiaries can still face out-of-network charges in some situations.

Now more than ever, working with a trusted Medicare expert ensures you’re prepared and protected. If you have any concerns about your coverage, schedule a call with Mark today to review your plan and avoid unexpected surprises.

-

UPDATE 8/1/2025: While the Bend and Salem offices remain on the government’s “wall of receipts” list of lease cancellations, no further information has been released regarding closure dates, and both offices remain open.

As announced at the end of last week, the federal government will be closing two out of three IRS offices in Oregon (Bend and Salem), leaving only the Portland location open. Here's how this affects Medicare and your retirement planning:

This will cause delays in verifying income, accessing tax records, or resolving financial matters tied to retirement planning.

Very specifically —> Less people on staff means less people available to process IRMAA (income related annual adjustment) appeals.

Social Security offices are already experiencing longer delays for Medicare enrollment and wait times for essential services are increasing. While these changes are out of our hands, what we can do is help you navigate them:

Start now - If you are nearing 65 or planning for retirement, taking action early is no longer "just good advice"—it is essential to ensuring a smooth transition to Medicare.

Check out our FAQ page for details on planning.

Get expert help - These larger system changes reinforce why having a trusted expert on your side makes all the difference.

Schedule a call - it's ok to just ask a question; there is no minimum knowledge required and no obligation to take any action. We're here to help, always.

-

We’re going to make this direct, and as clear as possible: Start as early as you can enrolling into Medicare Parts A & B. Time is not necessarily on your side, and here’s why:

Social Security offices are currently not taking walk-ins.

Phone hold times with Social Security are stretching several hours.

In-person appointments are being booked several months out.

Why this matters:

A quick turnaround once you’ve submitted is not guaranteed; waiting too long to apply for A & B could mean a delay in obtaining coverage, some of which could include penalties.

You need to have Part B before you can enroll in either a Medicare Supplement with Part D or a Medicare Advantage plan.

The sooner you take action, the more options you’ll have - and the smoother your transition to Medicare will be.

ALSO IMPORTANT - knowing ahead of time which coverage path is right for you (Medicare Supplement with a PDP or Medicare Advantage) is equally important. Given potential delays in obtaining Part B*, waiting to make these decisions can create unnecessary stress and limit your choices. Don’t do that to yourself! Book an appointment to map out your timeline. Avoid any avoidable problems that might come up. Medicare should be about peace of mind, not panic.

*We are not saying this WILL happen; we are saying it COULD happen, and to plan accordingly.

-

A lot happens behind the scenes in Medicare/insurance/healthcare that we never hear about. Increasingly, however, we ARE hearing about insurance companies and hospital systems renegotiating their contracts, because clients/patients receive letters notifying them of a negotiation in process and the potential for disruption in care if the negotiation is unsuccessful.

These can be disruptive, disconcerting, and alarming to receive.

Here are a few thoughts from where we sit as an entity independent of both the insurance companies and the hospital networks, though definitely within the crosshairs of the conversation:

We have seen several of these negotiations with companies over the last few years, and while it is stressful to receive the notices, it is required by CMS that they be sent, and negotiations themselves are not an unusual occurrence.

We do not get advance of ‘inside’ notice of these - our independence of all insurance companies is excellent for maintaining neutrality in recommending a fit for you; this also means we are not privy to internal communications within those companies.

We consistently keep ears to the ground for things like this and respond the best that we can - as soon as we hear of something, available information is posted to this website in the announcement bar of the homepage.

ACTIONS YOU CAN TAKE:

Schedule a call to cover your current situation and to put a plan in place should we need to pivot and look at other options: Click here to book.

Check our homepage often and follow the links to the source updates - this is the most current information we have, and we’ve made it available and easily accessible for you.

While we can’t control these negotiations, we can help you understand your options and navigate any potential disruptions.

Our commitment is to you, not the insurance companies, and our goal is always to ensure you have the coverage that fits your needs. We get how frustrating - and scary - these can be, and we will always work to keep the most current information available to you, both on the negotiations and on your options.